Written by: Andres Fernandez

January 12, 2021

“Forget the failures. Keep the lessons.”

With the new year underway, many resolutions and goals have been made, but have those goals specific enough. For example, many want to save money or better their credit for this year. How are you going to do that? It’s easy to say I want to save enough to buy a trip to Miami, but how much do you need to save weekly or monthly? What is the total amount you want to save and how are you willing to do that?

To accomplish any financial goals for 2021, you need to prioritize the steps it takes to crush them. Setting your goals is one thing, but transforming them into reality is another thing.

In 2021, it’s critical to set financial goals because they serve as a guide for how you manage your money. Your goal is to save money and stay committed to doing it, don’t waste money on things you don’t need. Trust me, you really didn’t need that new iPhone. This drives a positive behavior change and will be the foundation for a great 2021. We have listed 7 doable financial goals for 2021 that will help you and your business succeed, along with tips on how to keep them.

After you’ve decided and developed your goals, it’s time to do the work to achieve them. This is the step where many people fail. Let’s take a look at the steps you need to take to accomplish your financial goals for 2021.

With the coronavirus pandemic having impacted many parts of life this past year, it has recorded low interest rates, making this a prime time to refinance and lower your monthly payments. If you’re able to secure a better rate and more favorable terms, refinancing your business loan could save your money in the long run.

Lowering your loan payments and setting up better repayment dates would free up cash flow within your business. This will give you the opportunity to invest the extra funds in payroll, equipment, inventory or other aspects of the business.

In addition, if a loan refinance would positively impact your cash flow, a lender like ours could approve you for a larger loan amount based on your debt-service ratio, which measures whether you have enough cash to cover your debt. Getting approved for a larger loan amount could save you from taking out a second loan if you need additional funding for your business.

Having credit card debt gets to be really stressful if not paid on time. Consider making it a goal for 2021 to pay if off. These are two of the most common yet effective strategies to lower your credit card debt and better your FICO score.

Bonus

Saving for emergencies should be at the top of your financial goals for 2021 list. Having money set aside for unexpected expenses helps protect you from a financial crisis. The emergency fund should not only cover emergencies but expenses as well. Many business industries have seasonals where sales is at its lowest and highest, so knowing these trends and having the funds to protect yourself is life saving.

One of the easiest ways to build your savings is to automate your funds. Most employers allow you to divide your paycheck into different accounts. If not, you can likely set up automatic transfers with your bank.

Most financial experts recommend that you have the equivalent of at least 3-6 months worth of expenses in a savings account for emergencies. If this seems overwhelming, you begin by adding $200-500 a month until you are able to add more while still paying off your credit card debt or loans.

Having any amount set aside to help is better than nothing.

Any set of goals must have an “expiration date.” When do you want it and how realistically is it to achieve this goal?

There is a relationship between long term and short term goals. Often, achieving a long-term goal requires reaching a set of short-term goals.

For example, in order to buy a $960 mountain bike in four years (long-term), you will need to save $240 (medium-term) in each of the next four years, or $20 a month (short-term). Also, consider what you are going to do to achieve the $20 a month and so on. Have a definitive plan to stick to it!

Breaking long-term goals into medium- and short-term goals helps to make them seem achievable.

People really do not understand the importance of saving for retirement. I know you might be light-years away or right around the corner; why does it matter, i’m doing good now, why not later, right? NO!

Use 2021 to boost your contributions to your 401(k)s or HSAs, plan a comprehensive retirement goal, no matter your age or life stage. Take meaningful steps to boost your financial wellness. If your employer offers a 401(k) match, be sure you’re contributing enough to get the full match since it’s essentially free money. Also make sure you are aware of where your money is being invested in.

This is by far what I believe is the most important contribution your money should be going to. (Of course your credit card debt, but remember there’s a balance.)

Do not limit investing to retirement contributions. If you already have an emergency savings account, consider setting up another account to invest.

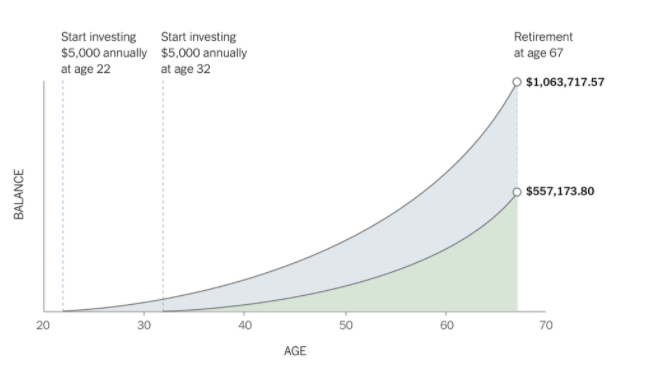

You’ve probably heard of the magic of compound interest. The best way is to see it for yourself.

If two people put the same amount of money away from each other ($5,000), earn the same return on their investments (6% annually) and stop saving upon retirement at the same age (67), one will end up with nearly twice as much money just by starting at 22 instead of 32. To put it another way: The investor who started savings 10 years earlier would have about $500,000 more at retirement.

Saving should be turned into a habit, just like it’s a habit to go out to eat every weekend to your favorite steak spot. It may make rational, mathematical sense to start saving as early as possible, but it isn’t always easy. But the instinct to save grows as you do it. It’ll begin to feel good as you see the balance on your account starts to grow.

Building multiple streams of income is no longer a luxury, it has become a necessity. If the high rate of unemployment throughout this last year and mounting job losses have taught us anything, it is that nobody’s job is safe. Unfortunately for most people, their only source of income is from their job, which can be a risky way to live. Some couples may be more fortunate and have a spouse bringing in money each month, yet still relying on their only source of income.

Each item listed below is an example of how alternative income sources can be used to lesson the risk of living on a single income.

Money drives almost all aspects of life. Getting in control of your financials is one of the most important things that you can do for yourself or your business. The first step is write down the goals you need to do to achieve the grand goal.

I hope you were able to gain some ideas and fundamental steps to get you started on the right track. Do not forget to check out our other resources we have.

You make decision when and how much you want to use your funds. As long as you have funds available, you can withdraw at anytime.

Withdraw from your line of credit whenever you want, as long there are funds available. You'll have the security to use whatever you need, wherever you are.

Capitalize customers have securely been funded over $3,000,000 directly to their bank account. Our application form, is highly secured so no information is hacked.

Capitalize Loans™ loans have simple terms ranging from daily, weekly, and monthly. No upfront fees or prepayment penalties. We provide you with a payment schedule before taking a loan so there won't be any surprises.

Securely link your last 3 month of bank statements to automatically get reviewed. This allows underwriters to evaluate your business right away and get approved fast.

Our team of experts are here to help when you need it, around the clock. We offer many ways to get in contact with us: phone call, email, text, and chat box is the fastest way to get ahold of us.